The rapid expansion of the CBD industry has created an urgent need for reliable payment solutions. Yet traditional payment processors often balk at CBD merchants. As you’ve built your CBD business, you’ve likely encountered repeated declines, sudden freezes, and sky-high fees that eat away at your profit margins. That’s where specialized CBD Online Payment Processing becomes essential to keep transactions flowing smoothly. In this blog, you’ll learn why mainstream payment platforms fail CBD entrepreneurs and how to secure compliant, cost-effective processing tailored to your needs.

The High-Risk Classification of CBD

When you launch a CBD venture, your first hurdle is risk classification. Financial institutions categorize CBD as high-risk because of its legal ambiguity and evolving federal and state regulations. This label triggers rigorous underwriting, restrictive policies, and hefty reserve requirements. As a result, traditional processors view CBD payments as too volatile, and you struggle to find a partner willing to process your transactions without excessive friction.

Legal and Regulatory Uncertainty

Even with the 2018 Farm Bill legalizing hemp-derived CBD at the federal level, the Food and Drug Administration (FDA) still restricts its use in food and supplements. Meanwhile, state laws differ on testing, labeling, and distribution, making compliance a moving target. In this patchwork landscape, payment processors hesitate to support CBD merchants whose operations may inadvertently cross regulatory lines.

Federal vs State Differences

While the federal government permits hemp-derived CBD under 0.3% THC, states like Idaho and Nebraska maintain tighter restrictions or outright bans. A processor authorized in California may be forced to freeze your account if you suddenly ship to a prohibited state. The lack of uniformity creates compliance risk, which many mainstream platforms refuse to shoulder on your behalf.

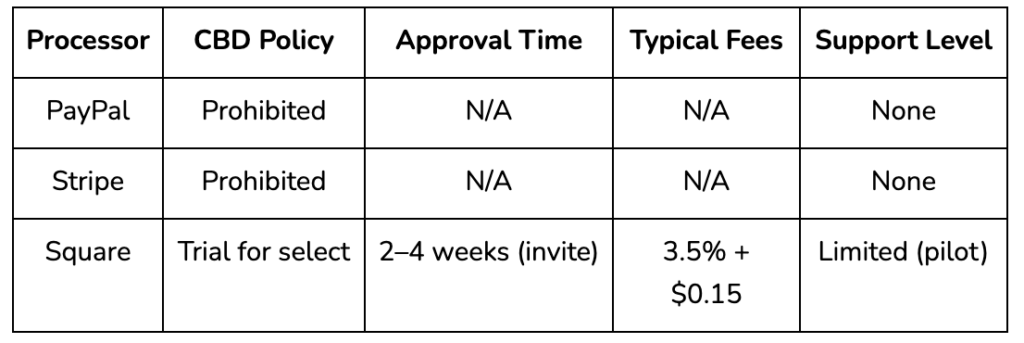

Why Traditional Payment Processors Fail CBD Merchants

Traditional processors such as PayPal, Stripe, and Square employ broad policies that exclude CBD merchants. These stakeholders rely on rigid rule engines and machine-learning algorithms that flag CBD transactions, triggering automatic declines or abrupt account terminations.

- Policy Restrictions Most mainstream processors have blanket bans on CBD sales. Their terms of service explicitly prohibit “high-risk” industries, and CBD falls squarely in that category. When you attempt to onboard, you face immediate denial of services.

- High Chargeback Rates CBD products often generate misunderstandings about dosage or effects, leading to disputes and chargebacks. Excessive chargeback ratios are a red flag for processors, who then hike your fees or close your account to avoid financial losses.

- Reserve Requirements If a processor grudgingly accepts your CBD business, you’ll likely encounter a rolling reserve. This means holding back 10–20% of your processed funds for 90–180 days. The cash-flow impact can cripple your inventory purchases and payroll.

- Compliance Overhead Payment processors invest heavily in Anti-Money Laundering (AML) and Know Your Customer (KYC) infrastructure. To protect themselves, they demand extensive documentation—proof of lab testing, COAs, licensing—then still reject CBD applicants when they perceive a compliance gap.

- Reputation Risks Even if your CBD operation is fully legal, traditional banks fear reputational damage from associating with an industry linked to cannabis. They’d rather deny your application than face scrutiny from conservative stakeholders or regulators.

Understanding CBD Merchant Account Risk

To overcome these barriers, you must grasp how risk impacts processing. Processors assign “risk scores” based on industry, chargeback history, and regulatory environment. High-risk categories incur greater underwriting scrutiny, elevated interchange-plus fees, and more rigid reserve mandates.

What Defines a High-Risk Merchant

A high-risk merchant is any business whose products or services are prone to chargebacks, regulatory scrutiny, or reputational concerns. Besides CBD, this includes gaming, adult entertainment, and overseas sales. For CBD merchants, the overlap of health claims, varying legal status, and fraud potential cements your high-risk profile.

How Risk Scoring Impacts Fees

Processors offset their risk exposure by adding percentage points to interchange rates and charging monthly account maintenance fees. A typical interchange-plus structure might run 1.8% + $0.10 for low-risk merchants, but for CBD you’re staring at 2.5–3.5% + $0.30 per transaction. Over thousands of orders, these hidden costs erode your margins and hinder scaling.

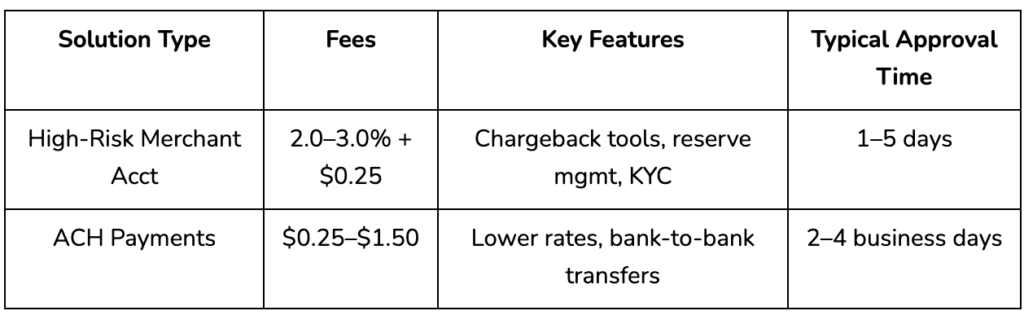

Alternative Payment Solutions for CBD Businesses

Fortunately, the high-risk ecosystem has matured. Specialized providers offer High-Risk Payments solutions designed for CBD entrepreneurs. These processors understand the FDA’s CBD guidelines, state-by-state regulations, and industry nuances. They package services like fraud prevention, chargeback mitigation, and multi-channel integration at transparent rates.

You can also diversify your payment methods beyond cards. Automated Clearing House (ACH) transfers, e-wallets, and even cryptocurrency acceptance reduce dependence on high-fee card networks. Incorporating an omnichannel strategy with a reliable payment gateway ensures you never lose a sale due to processor limitations.

How to Secure a CBD Merchant Account Approved Fast

Securing processing quickly hinges on preparation. First, ensure your business documents are in order: Articles of Incorporation, EIN, valid merchant license, and state hemp registration. Next, publish a fully compliant website with clear refund policies, privacy statements, and disclaimers. Present third-party lab results (COAs) prominently to demonstrate product legitimacy.

Then, partner with a specialized provider that streamlines underwriting. By choosing a processor familiar with your vertical, you cut approval times to as little as 24–48 hours. If speed matters, look for a CBD Merchant Account Approved Fast guarantee. This approach minimizes downtime and keeps your cash flow uninterrupted.

Role of Fraud Prevention and Chargeback Management

Even with specialized processing, you must actively manage fraud and disputes. Implement Address Verification Service (AVS), Card Verification Value (CVV) checks, and velocity limits to flag suspicious behavior. Use real-time transaction monitoring to detect anomalies, and maintain transparent communication with customers to resolve issues before they escalate.

A robust chargeback management platform can automate your rebuttal letters, archive supporting documents, and track dispute outcomes. Over time, a low chargeback ratio improves your risk score, leading to better rates and fewer reserves.

Leveraging High-Risk Payments Platforms to Reduce Denials

When you switch to a high-risk platform tailored for CBD, you gain a partner rather than just a vendor. These platforms maintain banking relationships with acquirers that understand hemp compliance, so your transactions sail through without generic risk flags. They also offer dedicated account managers who guide you through state license renewals, FDA updates, and seasonal promotional spikes to preempt denials.

Conclusion – Embrace Specialized Payment Solutions

Traditional payment processors were built for low-risk industries and cannot accommodate the unique demands of CBD merchants. From blanket bans and high chargeback fears to onerous reserves and compliance burdens, mainstream platforms impede your growth. By shifting to a specialized high-risk payment provider and obtaining a CBD Merchant Account Approved Fast, you can secure the reliable, scalable processing your CBD business deserves.

Ready to end transactional roadblocks? Cathedral Payment is here to empower your operations with compliant, competitive, and lightning-fast CBD payment solutions.

FAQs

1. What makes CBD a high-risk merchant category?

CBD’s high-risk status stems from regulatory ambiguity, elevated chargeback potential, and reputational concerns due to its cannabis origins.

2. Why do processors deny CBD credit card payments?

Traditional processors have blanket policies against CBD, fearing legal exposure, compliance complexity, and excessive chargebacks.

3. How can I lower fees on CBD merchant accounts?

Partner with a specialized high-risk processor offering interchange-plus pricing, volume discounts, and flexible reserve arrangements.

4. What documents are needed for fast CBD payment approval?

You need a valid business license, EIN, Articles of Incorporation, state hemp registration, compliant website documents, and third-party lab reports.

5. Can I process CBD payments without a merchant account?

Yes. You can offer ACH transfers, e-wallets, and cryptocurrency options, but these alone may not suffice for your entire customer base.