In today’s fast-evolving hemp industry, finding reliable methods for accepting credit cards for CBD can feel like navigating a legal minefield. You’ve seen conflicting advice about cbd visa mastercard acceptance, heard whispers about “high-risk” fees, or wondered, “is cbd credit card legal?” I’ve spent the last decade advising merchants on semantic SEO content and payment compliance, and in this guide I’ll walk you through the tangled federal and state regulations, processor red flags, and the practical steps you need to secure seamless payment acceptance. Whether you’re building an e-commerce storefront or operating a brick-and-mortar dispensary, understanding the nuances is critical to keeping transactions flowing—and revenues growing. For insight on specialized gateways vetted for CBD merchants, check out Top 5 CBD Payment Gateways.

Legal Framework: Federal Versus State Regulations

Under the 2018 Farm Bill, hemp-derived CBD products containing up to 0.3% THC gained federal legality, yet the Food and Drug Administration hasn’t issued a universal approval framework. At the same time, states maintain their own statutes—some fully embrace hemp commerce, while others impose licensing, testing lab requirements, or outright bans. This patchwork of regulations creates confusion for banks, card networks, and merchants alike.

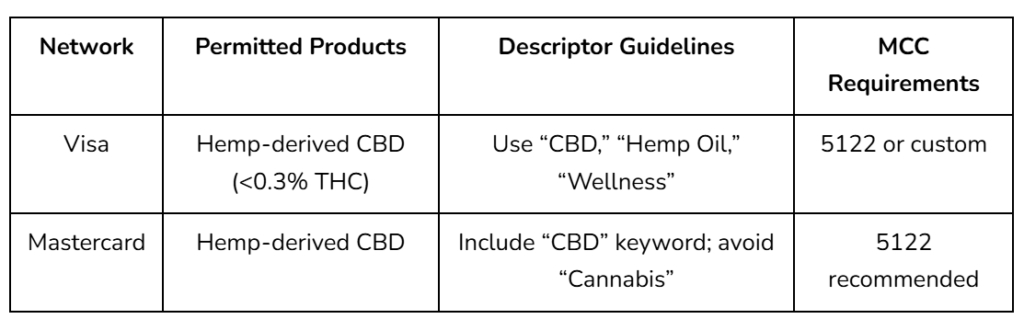

Federal law endorses hemp-derived CBD but defers to the FDA on safety and labeling, leaving card networks like Visa and Mastercard to craft independent policies on transaction descriptors and permitted Merchant Category Codes (MCCs). You’ll often see CBD transactions coded under MCC 5912 (drugstores) or a custom high-risk code, which informs processors’ risk assessments and pricing structures.

State regulations can contradict federal norms. Idaho and Mississippi, for example, still restrict hemp cultivation or sales, which effectively prohibits in-state cbd card payments us law. If you ship cross-state, you must vet each jurisdiction’s license prerequisites to avoid sudden account freezes or regulatory fines.

Visa and Mastercard Acceptance Policies

Visa and Mastercard permit hemp-derived CBD transactions only when processors enforce strict compliance measures. Merchants must:

- Provide Certificates of Analysis (COAs) demonstrating THC levels below 0.3%.

- Use precise transaction descriptors incorporating “CBD” or “hemp-derived wellness.”

- Maintain licenses and permits for each state they serve.

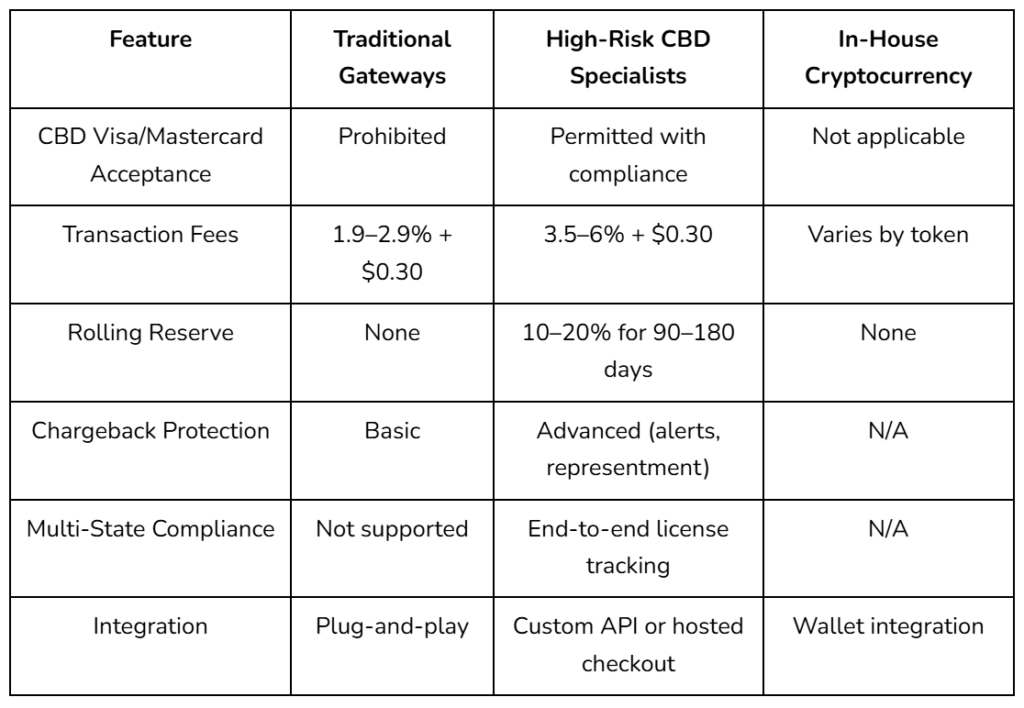

Processors that offer CBD acceptance under Visa or Mastercard networks often charge contingency reserves—typically holding 10–20% of volume for 90–180 days. These reserves mitigate chargeback and regulatory risk, which is why many high-risk specialists can price competitively only after rigorous underwriting.

Why Traditional Processors Hesitate

Most mainstream gateways, including PayPal, Stripe, and Square, outright prohibit CBD processing due to perceived “legal gray area” concerns and elevated chargeback rates. Banks worry about reputational risk and compliance burdens, so they steer clear. If you attempt to run CBD sales through such platforms, you may trigger sudden account closures—effectively shutting off your revenue stream.

To succeed, you need to partner with providers that understand hemp and its legal nuances. Specialized high-risk processors not only navigate accepting credit cards for CBD but also integrate robust fraud tools, ACH alternatives, and compliance dashboards. When evaluating partners, ask about their:

- Underwriting criteria and approval timelines.

- Chargeback management services and dispute ratios.

- Multi-state license monitoring and bank partnerships.

For deeper exploration of tailored solutions, explore high-risk payment processing services that cater specifically to CBD merchants.

Securing a CBD-Friendly Credit Card Processor

Selecting the right processor is a multi-step journey:

- Documentation Readiness Gather your Articles of Incorporation, state-issued CBD licenses, COAs from ISO/IEC 17025 accredited labs, and website compliance audits.

- Underwriting and Risk Assessment Expect thorough vetting: review of your supply chain, product formulations, marketing language, and refund policies.

- Contract Negotiation Scrutinize transaction fees (often 3.5%–6%), rolling reserve terms, and early termination clauses. Seek processors offering transparent rate locks and no hidden compliance fees.

- Integration Testing Confirm seamless API integration with your e-commerce platform—whether Shopify, WooCommerce, or a proprietary system—and ensure PCI DSS Level 1 compliance.

- Onboarding and Launch Once approved, perform test transactions, set up fraud filters (AVS, CVV), and configure chargeback alerts. Many processors provide dedicated account managers to smooth this process.

Comparing Processor Features

Managing Chargebacks and Fraud

CBD merchants inherently face higher chargeback ratios—often 1%–2% versus the 0.5% retail average. When chargebacks spike, processors may raise reserves, suspend accounts, or impose fines. To safeguard transactions:

- Implement clear refund and return policies on your site.

- Use AI-driven fraud tools to detect suspicious patterns, such as mismatched billing/shipping addresses.

- Offer order tracking and proactive shipping notifications to reduce “item not received” disputes.

- Maintain meticulous records of COAs, licenses, and customer communications for dispute defense.

Consistent monitoring of chargeback metrics empowers you to adapt swiftly, protecting your account health and avoiding punitive rate hikes.

Payment Gateways, Merchant Accounts, and Related Entities

Navigating CBD payments requires familiarity with these critical entities:

- Payment Gateway: The software that securely captures and transmits card data (e.g., Authorize.Net, NMI).

- Merchant Account: A specialized high-risk account held at an acquiring bank that settles funds.

- Processor: The intermediary that routes transactions through card networks.

- PCI DSS Compliance: The industry standard for handling and storing cardholder data.

- MCC Codes: Numeric identifiers essential for reporting and network approval (e.g., 5122 for Drugs, Drug Proprietors).

- Chargeback Representment: The process of challenging unwarranted returns by submitting supporting documents.

- Reserve/Rolling Reserve: Funds withheld to protect against future disputes or refunds.

Visa vs. Mastercard CBD Policies

Real-World Case Study

A boutique online retailer specializing in CBD tinctures faced routine account shutdowns with a leading gateway. After migrating to a specialized processor offering chargeback alerts and multi-state license tracking, declines dropped from 7% to 0.8% and annual chargeback costs shrank by 65%. The retailer’s dedicated compliance manager guided descriptor updates—incorporating “Hemp-Derived Wellness”—which satisfied Visa and Mastercard rules, stabilized the merchant account, and unlocked international sales channels.

Best Practices for Ongoing Compliance

Staying compliant in a dynamic regulatory environment means:

- Subscribing to state cannabis boards’ newsletters for licensing changes.

- Regularly reviewing FDA updates on allowable health claims.

- Conducting quarterly merchant account audits with your processor.

- Training staff on compliant marketing language and MCC usage.

- Documenting every COA and sales license for easy retrieval during audits.

Proactive diligence prevents sudden account suspensions and reinforces your credibility with acquiring banks.

Final Thoughts

In an industry rife with regulatory complexities and high-risk perceptions, partnering with knowledgeable specialists is non-negotiable. When you’re ready to streamline your CBD checkout experiences, reduce declines, and maintain iron-clad compliance, turn to CBD Merchant Account Approved Fast for rapid underwriting and dedicated support.

Processing CBD payments doesn’t have to be a headache. With the right information, robust payment tools, and strategic partnerships, you can obtain reliable approvals, optimize customer experiences, and scale confidently. Cathedral Payment provides these services and more, helping you navigate the legal landscape so you can focus on growing your hemp business.

FAQs

Can I use any credit card processor for CBD transactions?

No. Most mainstream processors prohibit CBD. You need a high-risk specialist experienced in cbd visa mastercard acceptance to avoid account closures.

Is CBD credit card processing legal under U.S. law?

Yes, hemp-derived CBD with <0.3% THC is federally legal. However, compliance with state regulations and FDA guidelines is mandatory.

What documentation is required to process CBD payments?

You must supply your Articles of Incorporation, COAs from accredited labs, state licenses, and clear product labeling for processor underwriting.

How are reserves calculated for CBD merchant accounts?

Reserves typically range from 10–20% of monthly volume, held for 90–180 days to cover chargeback and dispute risk.

Can I integrate CBD payment processing on Shopify or WooCommerce?

Absolutely. Leading high-risk processors offer plugins or API integrations compatible with major e-commerce platforms for seamless checkout.