Securing a CBD merchant account used to feel like scaling a wall blindfolded. You needed to prove every facet of your business was above board, all while traditional financial institutions treated you as if you were a trafficker rather than an entrepreneur. In today’s high-risk environment, understanding CBD payment compliance and executing a fast CBD merchant onboarding strategy can mean the difference between stalled growth and processing orders the next day. I remember the first time I guided a hemp startup through underwriting. When we contrasted their success against industry horror stories, it became clear: aligning documentation, legal definitions, and process flows correctly unlocks rapid approvals. Along the way, I discovered that Traditional Payment doesn’t work for CBD Businesses and that you must partner with specialists who live in the high-risk lane.

In this comprehensive guide, I’m walking you through the same blueprint I’ve refined over a decade. We’ll unpack the regulatory framework, dive deep into processor requirements, share operational best practices for getting CBD approved fast, and spotlight every semantic entity from Certificate of Analysis (COA) to rolling reserves—you’ll encounter. By the final paragraph, you’ll have a clear roadmap to optimize your merchant application, skirt common pitfalls, and enter production with confidence. Let’s get started.

Why CBD Merchant Accounts Are Classified as High-Risk?

The term “high-risk” carries weight: elevated fees, rolling reserves, intermittent holds, and meticulous underwriting. CBD merchants face scrutiny because the federal stance on hemp shifted only recently with the 2018 Farm Bill, and states still maintain disparate regulations around sale, distribution, and age requirements.

CBD payments are lumped alongside tobacco, nutraceuticals, and gambling strictly due to perceived chargeback probability and regulatory complexity. Banks fear the unknown: what if THC levels spike? What if advertising crosses state lines? What protections exist against mislabeling or unverified health claims? This collective caution translates into swaths of unwelcome calls to your business, unless you speak the language of compliance fluently.

Regulatory Landscape and the 2018 Farm Bill

In December 2018, Congress removed hemp from the Controlled Substances Act, birthing a federally legal CBD market under 0.3% THC. But the U.S. Food and Drug Administration (FDA) still restricts ingestible health claims and mandates strict COA testing. At the state level, age verification, licensing, and transportation rules vary some states even require in-state lab certification for every SKU. Aligning to these layers of legislation is no small feat.

Bank Stigma and Chargeback Risks

Chargebacks drive banks to blacklist industries. When consumers misunderstand product efficacy or feel misled on potency, they initiate disputes. Each chargeback triggers processing fees, surcharge investigations, and sometimes, rolling reserves up to 20% of gross volume. High reserve rates, unexpected holds, and sudden account terminations are common if a merchant doesn’t mitigate these risks.

Core High-Risk Entities

Behind every clean approval lie several key semantic entities:

- Certificate of Analysis (COA): Third-party lab report confirming THC percentage and contaminant screening.

- Underwriting Scrub: A proactive review of merchant application to ensure no red flags on website, compliance, or financial history.

- Rolling Reserve: A bank-mandated percentage of daily processing withheld as a chargeback buffer.

- Interchange-Plus Pricing: A fee model offering transparency by splitting card network fees (interchange) and processor markup.

- Merchant Descriptor: The name printed on customer statements to reduce dispute rates.

- PCI DSS Compliance: Adherence to encryption, tokenization, and data security standards to protect cardholder data.

Understanding and mastering these concepts equips you to present your business in the best light to acquirers and high-risk specialists.

Core Requirements for Approval

A streamlined application complete, accurate, and categorized, cuts underwriting time sharply. Missing or vague documentation is the single largest cause of delayed approvals.

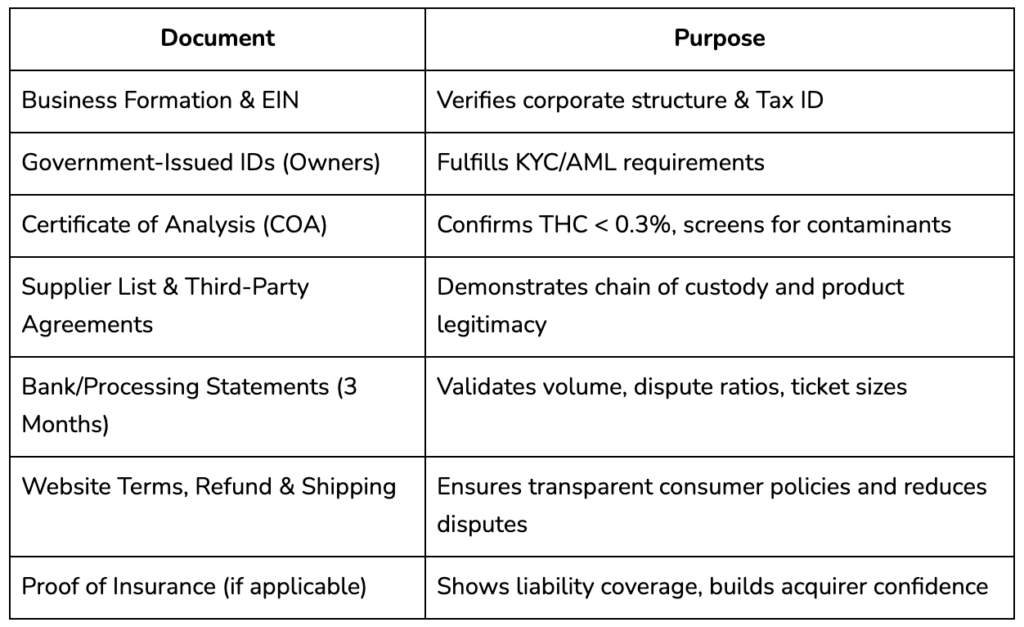

Business Documentation and KYC

Banks need to verify your identity and legitimacy. You’ll supply:

- Operating Agreement or Articles of Incorporation

- Employer Identification Number (EIN)

- Proof of Address (Utility Bill or Lease Agreement)

- Government-Issued Photo ID for Owners

These documents satisfy Know Your Customer (KYC) and Anti-Money Laundering (AML) mandates. If any detail conflicts, expect additional inquiries and a longer approval window.

Certificate of Analysis (COA) and Supplier Verification

Because CBD legality hinges on THC content, every product batch must carry a COA from an ISO/IEC 17025-accredited lab. The COA proves compliance with the 0.3% THC threshold and screens for heavy metals, pesticides, and microbial contaminants. Processor underwriters will often ask for the supplier’s COA, as well as a documented chain of custody or supplier list to validate every vendor in your supply chain.

Financial Statements and Processing History

If you’ve been processing through PayPal, Stripe, or a third-party facilitator, you need three months of processing statements. These help forecast volume, dispute ratios, and average ticket sizes. If you’re new to processing, your processor may request personal or business bank statements to assess risk and set reserve requirements accurately.

Website and Terms of Service Clarity

Underwriters will comb through your website. Ensure you:

- Disclose lab certification and COA access

- Avoid unapproved medical claims

- Clearly list terms & conditions, refund and shipping policies

- Implement age-gate or ID verification for online sales

Inconsistent or vague policies sow underwriting doubts, prompting manual reviews and delays.

Required Documents vs Purpose

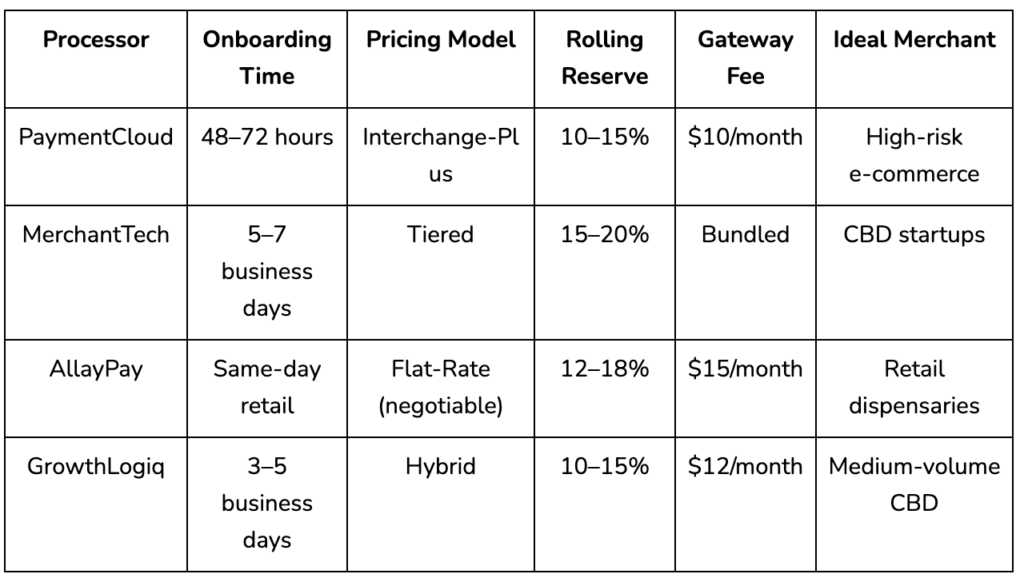

Choosing the Right Processor for Fast CBD Merchant Onboarding

Not all payment facilitators are structured to support cannabis-adjacent businesses. Selecting a provider who specializes in cbd processor requirements will spell the difference between “pending” and “approved.” Here’s what to look for.

Pricing Models: Interchange-Plus vs. Tiered vs. Flat-Rate

Interchange-Plus lists the actual interchange fee set by networks (Visa, Mastercard) plus a transparent markup. It’s ideal for high-volume merchants seeking predictable costs.

Tiered bundling obscures the true card network fees, grouping transactions into “qualified,” “mid-qualified,” or “non-qualified” buckets.

Flat-Rate charges a constant percentage, commonly used by payment aggregators but often penalizes high-volume or high-ticket sellers, raising effective fees.

Supported Sales Channels: Online, Retail POS, MOTO, Virtual Terminal

Your processor should offer a suite of solutions:

- E-commerce gateway with secure API integration

- Mobile & desktop Virtual Terminal (for phone orders)

- Point-of-Sale (POS) terminals certified for high-risk retail

- Mail Order/Telephone Order (MOTO) software for subscription services

When you integrate all channels under a single account, it simplifies reconciliation and risk monitoring.

In many cases, a provider may promise instant onboarding but lack the advanced features required for robust compliance. Always confirm whether they actively underwrite high-risk merchants or simply broker a sub-account model that can vanish at the first sign of chargebacks.

Once I switched to a processor with real high-risk expertise, my approval went through in 48 hours, no 30-day hold,” recalls a CBD skincare retailer I recently guided.

Midway through your evaluation, you’ll discover why CBD Online Payment Processing work more reliably with specialists who understand hemp products and federal requirements.

Operational Strategies to Accelerate Approval

Even with perfect documents, poor communication or misaligned descriptors can trigger red flags. Here’s how to position your application for the fastest decision.

Pre-Application Preparation

Before hitting “Submit,” compile every document into a single digital folder, clearly named. Create an application summary sheet listing all supporting docs and include it with your submission. This proactive transparency reduces clarifying questions and back-and-forth emails.

Underwriting Scrubbing and Consultation

A “pre-flight” scrub by a seasoned consultant identifies gaps: ambiguous TOS, incomplete COAs, or suppliers lacking credentials. Acting on these insights prior to submission often cuts the typical 10-15 business day turnaround in half.

Proper Merchant Descriptor and Categorization

The billing descriptor matters. A descriptor like “HempWellnessCo” or “TheraCBD Shop” reduces confusion compared to a generic “123456789 POS.” Align your descriptor exactly with your DBA (Doing Business As) name and website branding to minimize chargebacks.

Effective Communication with Acquirer

Designate a single point of contact for underwriting questions. Patchy, late-night responses from random team members prolong the process. Assign one liaison—ideally someone versed in your inventory, pricing, and compliance protocols—to field all queries until final approval.

Costs, Fees, and Funding Terms Explained

Now that your account is approved, get clear on the downstream implications. High-risk accounts often carry specialized fee structures.

Merchant Discount Rate (MDR) and Interchange

Your cbd payment compliance strategy must anticipate card network fee fluctuations. Each card brand’s interchange rate varies by card type, transaction volume, and merchant category code (MCC). The processor’s markup atop interchange dictates your final MDR.

Rolling Reserve and Chargeback Holdback

Banks typically withhold 10–20% of gross daily volume in a rolling reserve, released after a defined “rolling period,” often 180 days. Some providers offer reduced reserves if you hit specific dispute ratios, encouraging proactive chargeback management.

Gateway, Statement, and PCI Fees

Separate gateway fees apply if you route transactions through a third-party gateway. Statement fees (often $10–$20/month) and annual PCI compliance charges can gum up profitability if overlooked. Negotiating these line items can trim tens of thousands annually for mid- to large-sized operations.

Fee Structure Comparison Among Top Processors

Post-Approval Optimization: Fraud Prevention and Compliance

Approval is only the beginning. To maintain a stable processing relationship, you must stay vigilant against fraud and maintain strict cbd payment compliance.

PCI DSS and Tokenization

Ensure you complete the correct Self-Assessment Questionnaire (SAQ) level each year. Implement tokenization or vault services so that you never store raw card data on your servers, reducing your liability footprint.

3-D Secure, AVS, and CVV Checks

Activate 3-D Secure (Visa Secure, Mastercard Identity Check) to shift fraud liability. Match billing addresses with the Address Verification Service (AVS) and require CVV codes to block the majority of automated fraud attempts.

Chargeback Management Tools

Deploy real-time alerts and representment services. When a dispute arises, you’ll have 45 days to gather shipment records, proof of delivery, and contract acceptance to successfully challenge frivolous chargebacks.

By proactively addressing disputes, you can reduce chargeback ratios below the processor’s 1% threshold, which in turn lowers reserve requirements and opens doors to interchange-plus pricing discounts.

Partnership with a proactive chargeback management vendor often reduces merchant vulnerability by over 30%, ensuring smoother long-term funding.

State-by-State Considerations for High-Risk Merchants

Beyond federal law, each state can impose unique mandates on sale, shipping, age verification, and packaging.

Federal vs State Law Nuances

While the Farm Bill legalizes hemp, states like Idaho still ban THC products altogether. Oregon allows topicals containing up to 0.5% THC if labeled and packaged under farm-to-table processes. Navigating this mosaic demands dynamic compliance protocols.

Age Verification and Shipping Restrictions

Several states require age-gate popups or third-party age verification for all CBD orders. Florida mandates adult signature upon delivery, while Texas prohibits it entirely. A robust shipping partnership that flags restricted states in real time prevents accidental policy violations.

At this stage, consider a geo-fencing solution that automatically blocks checkout in prohibited regions, further insulating your merchant account from unexpected holds or account reviews.

Conclusion

Getting your CBD merchant account approved swiftly isn’t an accident, it’s the byproduct of strategic preparation, choosing the right high-risk partner, and mastering every layer of cbd processor requirements. From assembling ISO-accredited COAs to selecting interchange-plus pricing and implementing real-time fraud tools, each step we’ve covered accelerates underwriting and ensures stable funding.

At Cathedral Payment, we specialize in fast cbd merchant onboarding and comprehensive cbd payment compliance services. Our structured approach, deep high-risk expertise, and proprietary underwriting scrub process have enabled hundreds of hemp businesses to process online, in stores, and via phone within 72 hours. Ready to skip the gatekeepers and get approved fast? Cathedral Payment is here to make it happen.

Frequently Asked Question

1. How do I get a CBD merchant account approved fast?

Fast approval hinges on completeness. Submit a fully scrubbed application including business formation docs, COAs, supplier lists, financial statements, and clear website policies. Partnering with a specialist who pre-reviews your submission can reduce standard approval times from weeks to 48–72 hours.

2. What are the essential documents for CBD merchant underwriting?

Underwriters require your Articles of Incorporation (or DBA), EIN, government IDs, three months of bank/processing statements, supplier agreements, ISO-certified COAs for each SKU, and clear refund/shipping policies on your website.

3. How long does it take to set up an online CBD merchant account?

With a high-risk specialist like us, retail CBD accounts can be live in as little as 24 hours, and e-commerce integrations typically under 72 hours, provided all documents are accurate and complete.

4. Why is CBD merchant processing considered high-risk?

Complex federal and state regulations, THC content thresholds, chargeback frequency, and reputational concerns among banks drive the high-risk designation, resulting in higher fees and reserve requirements.

5. Can I switch from a traditional payment processor to a CBD-friendly provider?

Yes. You simply apply for a new account, maintain your existing merchant ID until cutover, then transition transaction flows to the new provider. Make sure to capture all historic data for dispute representation.