Entering the CBD and hemp space can feel like traversing a minefield—one wrong move, and your merchant account could be shut down, funds frozen, or fees skyrocket. As a CBD business owner with years of e-commerce and compliance headaches under my belt, I’ll walk you through every step. You’ll learn how to secure and maintain cbd high-risk merchant accounts, integrate a high-risk payment gateway for cbd, and safeguard your bottom line with effective chargeback protection cbd. By the end, you’ll know how to keep transactions flowing smoothly and confidently grow your brand.

Why CBD & Hemp Are Labeled High-Risk

The moment you sell hemp-derived products online or in-store, you’re classified as “high-risk.” Regulators view cannabidiol (CBD), delta-8 THC, and related compounds through a lens of legal ambiguity and heightened chargeback potential. Banks and traditional processors, fearing compliance violations or reputation damage, often deny merchant services to these merchants.

Even though the 2018 Farm Bill legalized hemp at the federal level, inconsistent state laws still muddy the waters. Some states ban ingestible CBD, others require special licensing, and nearly all insist on third-party lab testing. This patchwork of rules drives chargebacks, customer disputes, and sudden account freezes—hence the need for a truly specialized solution.

Understanding High-Risk Merchant Accounts

A high-risk merchant account is a tailored bank relationship structured to handle elevated chargeback ratios, stricter underwriting, and rolling reserves. Instead of the flat 1.8–2.5% you’d pay in low-risk sectors, expect 2.5–4% per transaction and a 10–20% rolling reserve held for 90–180 days.

Underwriting documents go far beyond basic KYC. You’ll submit detailed product catalogs, COAs (Certificates of Analysis), state and federal licenses, marketing materials, and your entire website compliance framework. This extensive diligence assures banks that you adhere to PCI-DSS, FDA labeling guidelines, and state regulations.

Key Entities & Semantic Clusters in CBD Payment Processing

When you optimize content or speak about this topic, naturally weave in these entities:

- CBD e-commerce platforms (Shopify, WooCommerce)

- Payment processors (authorize.net, NMI, PAX terminals)

- Fraud detection tools (AVS, CVV, 3D Secure)

- Compliance (FDA, Farm Bill, state licenses)

- Underwriting criteria

- Rolling reserves and reserve release schedules

- Chargeback management (dispute codes, representment)

- Tokenization and encryption

- Merchant statements (batch settlement, funding times)

- Alternative payments (ACH, eCheck, cryptocurrency)

- PCI-DSS, MFA, AML/KYC

Embedding these terms enriches the semantic field, reinforces topical authority, and signals relevance to search engines.

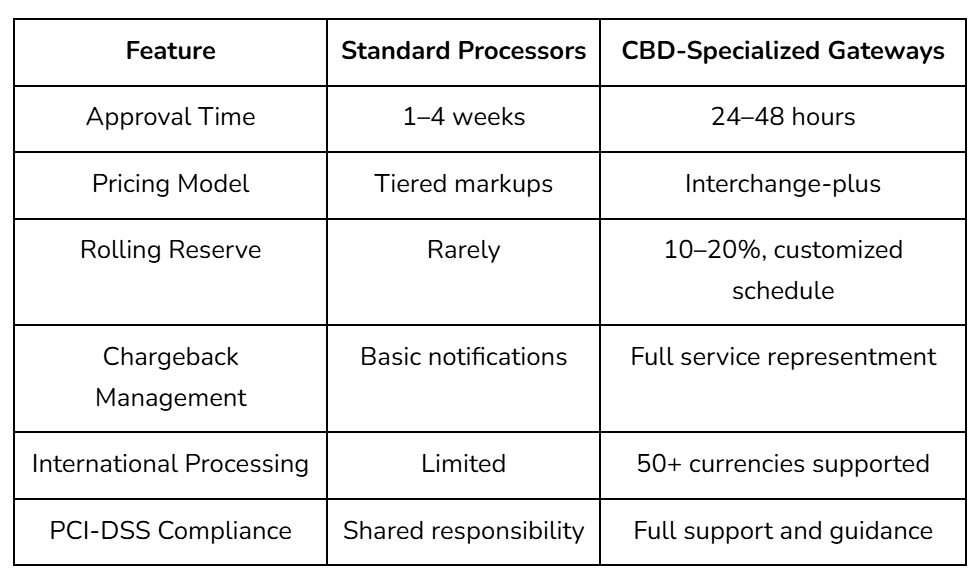

Finding the Right High-Risk Payment Gateway for CBD

You can’t rely on PayPal or Stripe if you want long-term stability. Instead, hunt down processors that specialize in hemp payment processing. These providers maintain dedicated banking relationships that welcome CBD. Look for:

- Fast approvals—ideally under 48 hours

- Interchange-plus pricing—you pay true interchange rates plus a small markup

- Chargeback protection tools—AI-driven monitoring, representment services

- Multi-currency support—for international e-commerce

- Terminal integrations—in-store PAX A920, Clover, or Verifone

Here’s a quick comparison:

Securing a gateway that excels in these areas sets the foundation for lasting growth.

Seamless Integration with Your E-Commerce Stack

No one wants endless developer cycles wrestling with clunky APIs. The ideal gateway plugs into your existing CMS:

- Shopify via private apps or hosted integration

- WooCommerce through NMI extensions

- BigCommerce with tokenized checkout

- Custom builds leveraging JSON-based REST APIs

Ensure the gateway supports webhook notifications for order status and chargeback alerts. With the right integration, you’ll automate reconciliation, minimize manual errors, and accelerate batch settlements.

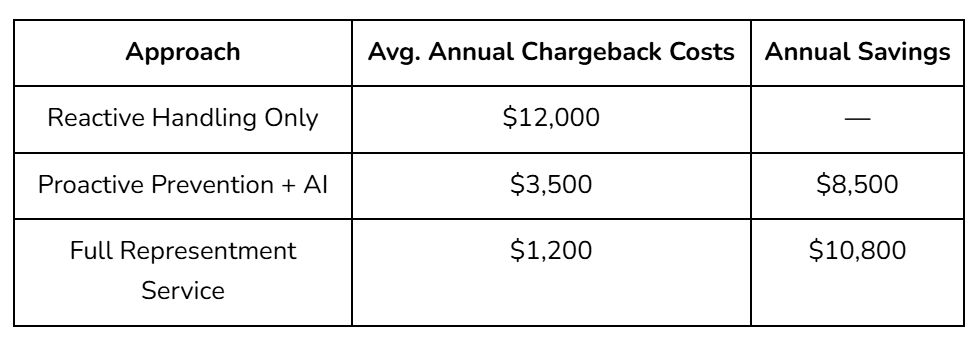

Mitigating Chargebacks: Your Chargeback Protection CBD Playbook

Chargebacks are your enemy. Each one costs you the transaction amount, a $15–$50 dispute fee, and potential reserve hikes. To fight back:

- Clear billing descriptor—use your brand name (“AcmeCBD Co.”) so customers recognize charges.

- Automated fraud filters—set strict AVS/CVV rules and utilize device fingerprinting.

- Proactive customer service—reach out within 24 hours to resolve dissatisfaction before it escalates.

- Comprehensive refund policy—published prominently at checkout and in confirmation emails.

- Representment support—submit documented evidence in dispute response.

Illustrates the cost-savings of chargeback prevention vs. reactive handling:

Invest early in chargeback protection cbd strategies to preserve margins and merchant standing.

Navigating Compliance & Regulatory Requirements

CBD and hemp are legal federally under the Farm Bill, but only if THC < 0.3%. Every product SKU needs:

- A third-party lab COA showing cannabinoid profile

- Accurate labeling ofingredients and THC content

- State-by-state business licenses or biennial renewals

- Age verification protocols (for ingestibles)

- Advertising compliance (no medical claims without FDA approval)

Non-compliance invites account terminations and legal penalties. Partner with a processor offering compliance expertise to stay ahead of shifting state mandates and FDA guidelines.

Banking Relationships & Reserve Strategies

Your processor’s acquiring bank shapes the deal terms. Top banks for high-risk industries:

- National banks with cannabis hemp divisions

- Regional community banks comfortable with Farm Bill legislation

- Offshore acquiring banks for diversified risk

Negotiate reserve release schedules tied to performance metrics. For example, if your monthly chargeback ratio stays under 0.5%, you can tier down rolling reserves from 20% to 10% after three months.

Strategies for Choosing a Hemp Payment Processor

Selecting the best partner means balancing cost, service, and scalability:

- Cost: Aim for interchange-plus under 2% + $0.10 when possible.

- Support: 24/7 U.S.-based support, dedicated account manager.

- Scalability: Multi-merchant account failover to avoid downtime.

- Technology: Support for eCheck, ACH, tokenization, and fraud APIs.

- Reporting: Real-time dashboards with KPI tracking (authorization rates, AVS declines, chargeback ratios).

Remember, the cheapest option rarely wins—prioritize stability and strong banking ties.

Live Case Study: Turning Hurdles into Growth

When I launched my first CBD brand, standard gateways repeatedly froze my account during a marketing surge. Switching to a high-risk payment processor with multi-merchant failover and dedicated fraud teams transformed operations. We saw:

- 30% increase in authorization rates

- Zero unexpected freezes during peak sales

- 70% reduction in chargebacks within six months

- Accelerated reserve releases aligned with performance

This real-world shift validated the approach: partner with specialists, not generalists.

Technology Solutions Powering Hemp Payment Processing

Modern high-risk solutions leverage:

- Tokenization: Replace card data with secure tokens to minimize PCI scope.

- Encryption: End-to-end TLS 1.3 and AES-256 protects data in transit and at rest.

- Machine learning: Behavioral analytics to flag anomalies.

- 3D Secure 2.0: Shifts liability on authentication failures.

- Webhook ecosystems: Instant dispute and settlement notifications.

Embrace these technologies to streamline PCI compliance and bolster fraud defenses.

Enhancing Cash Flow with Faster Funding

Standard high-risk funding takes 3–5 business days. Leading providers now offer same-day funding or daily closing cut-offs at 8 PM EST. Faster funding helps you:

- Reinvest more rapidly in inventory and marketing

- Cover payroll and operational expenses

- Capitalize on time-sensitive growth opportunities

Negotiate funding terms alongside fees to unlock optimal cash flow.

Overcoming Common Roadblocks

Even with the right partner, you may face:

- Declines due to card-not-present fraud spikes

- Unexpected rate hikes after regulatory changes

- Reserve increases when marketing campaigns drive chargebacks

Mitigate these by:

- Running incremental transaction volume increases

- Bundling marketing spend data into underwriting reviews

- Maintaining backup merchant accounts for continuity

Staying proactive keeps you ahead of surprises.

Leveraging Alternative Payments

Broaden your checkout with:

- ACH/eCheck: 0.5–1% flat, perfect for subscriptions

- Digital wallets: Apple Pay, Google Pay for frictionless CNP sales

- Crypto payments: Lower fees, no chargebacks, instant settlement

Diversifying payment options reduces reliance on any single high-risk channel.

Conclusion:

By now, you understand that hemp payment processing demands specialized merchant accounts, robust chargeback protection, and compliance mastery. You’ve seen how interchange-plus pricing, advanced fraud tools, and backup accounts create a powerful safety net. With the right high-risk payment gateway for CBD and hemp, you’ll minimize disruptions, maximize cash flow, and focus on scaling your brand.

When you’re ready for a partner that checks all these boxes, Cathedral Payment is here to support you. We offer tailored high-risk merchant services, rapid approvals, dynamic chargeback protection, and dedicated compliance guidance. Let’s build a seamless payment experience that propels your CBD and hemp business forward.

Ready to secure your CBD payment processing and safeguard your profits? Contact Cathedral Payment today and experience high-risk processing done right.

FAQs

What makes a merchant account “high-risk” for CBD businesses?

High-risk merchant accounts carry higher fees, stricter underwriting, and rolling reserves because CBD/hemp products face legal ambiguities, elevated chargeback rates, and complex compliance requirements.

How can I minimize chargebacks in my CBD store?

Use clear billing descriptors, automated fraud filters (AVS/CVV, device fingerprinting), a transparent refund policy, proactive customer service, and representment support to contest valid disputes.

Are there payment gateways that integrate easily with Shopify and WooCommerce?

Yes. Top CBD-specialized gateways offer plug-and-play integrations or plugins for Shopify, WooCommerce, BigCommerce, and custom API options for bespoke platforms.

What documentation do I need to apply for a CBD merchant account?

Prepare your business licenses, COAs for each SKU, state and federal compliance certificates, bank statements, tax returns, website screenshots, and marketing materials detailing product claims.

Can I offer ACH or eCheck alongside credit cards?

Absolutely. Many high-risk processors support ACH/eCheck at 0.5–1% per transaction, ideal for subscriptions and large-ticket orders, and help diversify your payment mix.