The Visa Acquirer Monitoring Program (VAMP) has long been a critical tool for Visa in managing and monitoring high-risk payments related to chargebacks and fraud. This program, which applies to both merchants and acquirers, has undergone significant changes. Understanding these changes is crucial for high-risk merchants, as it empowers them to ensure compliance and navigate the evolving landscape of payment processing. As of 2025, these changes introduce new thresholds, metrics, and monitoring procedures designed to streamline dispute resolution while enhancing fraud detection and prevention. In this post, we’ll dive deep into the latest updates to VAMP and explore the key differences between VFMP vs. VAMP, the importance of early warning alerts, and what the 2025 compliance requirements mean for merchants in high-risk industries.

What Is the Visa Acquirer Monitoring Program (VAMP)?

Visa’s Acquirer Monitoring Program (VAMP) is a global initiative designed to monitor the chargeback and fraud performance of merchants. The program plays a vital role in maintaining the integrity and security of the global payment system, providing high-risk merchants with a sense of security and reassurance. Under VAMP, Visa tracks key metrics, including dispute ratios, fraud levels, and the overall performance of merchants and their acquiring banks.

The purpose of VAMP is to identify merchants whose dispute or fraud rates exceed acceptable thresholds. When a merchant’s chargeback or fraud levels are too high, it signals to Visa that they are at an elevated risk of fraud or may be involved in activities that could harm the payment ecosystem. In these cases, Visa applies corrective measures, such as issuing penalties or putting the merchant under increased scrutiny. As of 2025, Visa has consolidated its multiple fraud and dispute monitoring programs into a single, unified system.

Key Changes Under the New Visa Acquirer Monitoring Program

1. Unified Dispute and Fraud Monitoring

The most significant change under the updated Visa Acquirer Monitoring Program is the unification of fraud and dispute monitoring. Previously, Visa had separate programs for fraud (the Visa Fraud Monitoring Program (VFMP)) and conflicts (the Visa Dispute Monitoring Program (VDMP)). With the new structure, these two elements are now monitored within a single system, simplifying the process for both merchants and acquirers.

This consolidation has led to the introduction of a combined fraud threshold of 0.9%, along with dispute monitoring. Merchants and acquirers will now be held to a single standard for both fraud-related and non-fraud disputes, making it easier to track compliance and potential violations. This change is significant for high-risk merchants in industries such as subscription services, digital goods, or adult content, where fraud and disputes are more prevalent.

2. Introduction of the Enumeration Ratio

One of the most notable new metrics introduced in VAMP is the enumeration ratio, which is designed to detect card testing or enumeration activities. Enumeration is when fraudsters attempt multiple card numbers to test whether they are valid, typically to make fraudulent transactions.

If more than 20% of a merchant’s transactions are identified as enumeration attempts, this will trigger an alert under the Visa Acquirer Monitoring Program. Merchants must be diligent in monitoring their transactions to detect and mitigate these types of activities, as failing to do so can lead to penalties or account suspension.

3. Revised Fraud and Dispute Thresholds

Visa has introduced new fraud and dispute thresholds that will directly impact high-risk merchants. These revised thresholds are designed to enhance the accuracy of monitoring and ensure that merchants maintain healthy dispute-to-transaction ratios.

- Fraud Threshold 0.9%: For early warning alerts, Visa has set a new fraud threshold of 0.9% for card-present and card-not-present transactions. Exceeding this threshold will result in penalties and further scrutiny from Visa. Merchants in sectors prone to fraud, such as e-commerce or subscription-based services, will need to focus on reducing fraudulent chargebacks to stay below this new threshold.

- Dispute Ratio Thresholds: Similarly, the acceptable dispute ratio thresholds have been revised:

- 2.2% by June 2025

- 1.5% in major regions such as North America, the EU, and Asia Pacific by April 2026

- 0.3% for acquirers, starting January 2026.

Merchants who exceed these thresholds risk severe consequences, including higher fees and even termination of their merchant accounts.

4. Enhanced Early Warning Alerts

With the latest updates to VAMP, Visa has introduced early warning alerts to notify merchants when they are approaching critical thresholds for chargebacks or fraud. These alerts provide merchants with an opportunity to take corrective actions before facing penalties, empowering them to be proactive and in control of their risk management. Early warning alerts are particularly crucial for high-risk merchants, who may face higher-than-average chargeback rates due to the nature of their business.

These alerts help merchants identify potential issues early in the process, allowing them to respond proactively. By focusing on early warning alerts, merchants can take steps to reduce fraud, improve customer service, and ultimately prevent chargeback ratios from exceeding Visa’s acceptable levels.

Key Differences: VFMP vs. VAMP

Before we dive into the compliance details for 2025, it’s important to understand the key differences between the previous Visa Fraud Monitoring Program (VFMP) and the current Visa Acquirer Monitoring Program (VAMP).

The VFMP focused exclusively on detecting and managing fraud within the Visa payment ecosystem, while the VAMP combines both fraud and dispute monitoring into a single system. This unified approach streamlines the management of chargebacks and fraud across different merchant types. For high-risk merchants, the VAMP’s comprehensive approach provides a more complete picture of their risk exposure.

Additionally, under the new VAMP, Visa monitors not just fraud but also general disputes, giving a clearer view of a merchant’s performance across all risk metrics. VFMP was primarily concerned with fraud prevention, whereas VAMP now encompasses a broader range of performance indicators.

Impact of VAMP on High-Risk Merchants

High-risk merchants, particularly those in industries such as e-commerce, digital content, gambling, and subscription services, are particularly vulnerable to chargebacks and fraud. The changes introduced by Visa will have a significant impact on how these businesses manage and respond to disputes.

With stricter fraud and dispute thresholds, merchants in high-risk sectors must be more diligent than ever in monitoring their transactions and managing disputes. If a merchant fails to comply with Visa’s rules, they risk penalties, increased fees, and even losing their ability to process payments through Visa.

For example, a fraud threshold of 0.9% means that if a high-risk merchant’s fraud rate exceeds this amount, Visa will flag them, and potential penalties will be enforced. The key to navigating this challenge is ensuring robust fraud detection systems are in place, such as using chargeback mitigation services, AI-powered fraud detection, and real-time alerts.

Note: You can also study in detail about Mastercard’s 2025 Chargeback Limits here

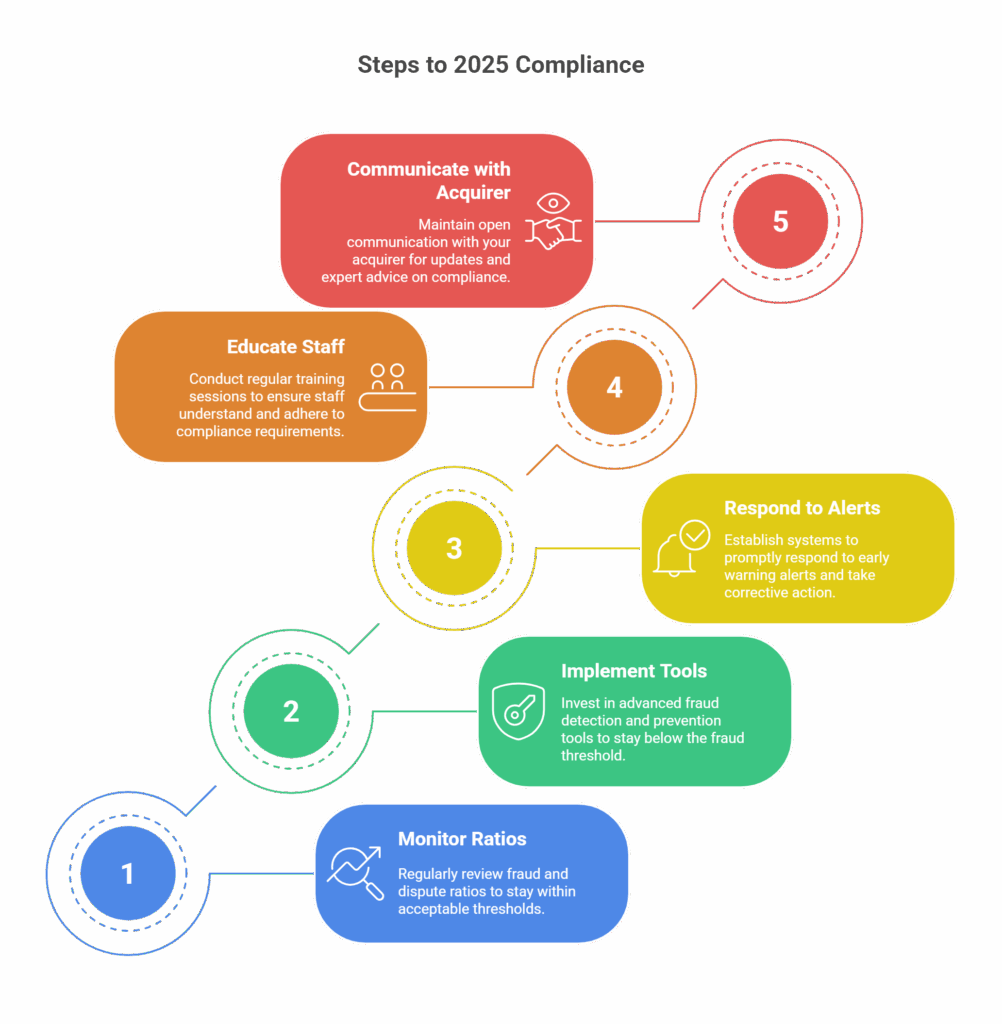

Steps to Ensure 2025 Compliance

For high-risk merchants, compliance with Visa’s new rules in 2025 is essential for maintaining operational continuity and avoiding costly penalties. Here are the key steps that merchants must take to ensure they remain compliant:

- Monitor Fraud and Dispute Ratios: The first step in ensuring compliance with VAMP is regularly reviewing your fraud and dispute ratios. Merchants should track these metrics closely to ensure they stay within Visa’s acceptable thresholds.

- Implement Advanced Fraud Prevention Tools: To stay below the 0.9% fraud threshold, merchants should invest in advanced fraud detection and prevention tools. These systems can help identify and block fraudulent transactions before they result in chargebacks.

- Respond quickly to Early Warning Alerts: Early warning alerts are an essential part of the updated VAMP rules. Merchants should establish systems to respond to these alerts promptly and take corrective action before critical thresholds are exceeded.

- Educate Your Staff: It is crucial that your team is educated on the new VAMP rules and understands the importance of chargeback prevention and fraud management. Regular training sessions and updates will ensure everyone is aligned with the latest compliance requirements.

- Maintain Open Communication with Your Acquirer: Work closely with your acquirer to ensure you’re staying informed about any changes to Visa’s rules and get expert advice on compliance strategies.

Conclusion

The updated Visa Acquirer Monitoring Program (VAMP) introduces several significant changes that high-risk merchants must be aware of. These changes, including the introduction of a unified dispute and fraud monitoring system, the establishment of an enumeration ratio, and revised thresholds, are designed to streamline the prevention of fraud and the resolution of disputes. By proactively managing their fraud threshold of 0.9%, implementing robust fraud detection tools, and responding to early warning alerts, merchants can stay compliant and continue to process payments seamlessly through Visa.

Stay under fraud and dispute thresholds. Align with both VFMP and VAMP. Integrate early warning alerts. Build a culture of 2025 compliance across your operations. And most importantly, a partner with experts who understand this landscape inside and out.

Cathedral is your trusted high-risk payments ally. Let’s simplify compliance, together.