Entering 2025, I’ve seen the CBD industry explode, nearly 30% annual growth over the past five years and with that boom comes one enduring headache: getting paid. Suddenly, merchant accounts that once welcomed me with open arms now slam the door shut the moment they see “CBD.” Today, I’ll walk you through what really works for CBD Online Payment Processing, what falls flat, and how you can win approval for your online CBD business payments.

Why CBD Payment Processing Remains High-Risk

I remember when accepting credit cards for hemp tinctures was as easy as installing a plugin. Fast-forward to 2025, and traditional gateways flag CBD as high-risk, sometimes grouping it with gambling or tobacco.

The root causes?

- Evolving regulations across states and countries that blur legality.

- FDA still finalizing guidelines on health claims and THC content.

- Banks and acquirers wary of chargebacks and compliance fines.

This high-risk label isn’t a passing fad. It affects your processing rates, underwriting standards, and even whether you can capture payments at all.

What Works: Specialized CBD Payment Solutions

Over the past decade, I’ve tested dozens of payment processors. Three core approaches consistently deliver for online CBD businesses:

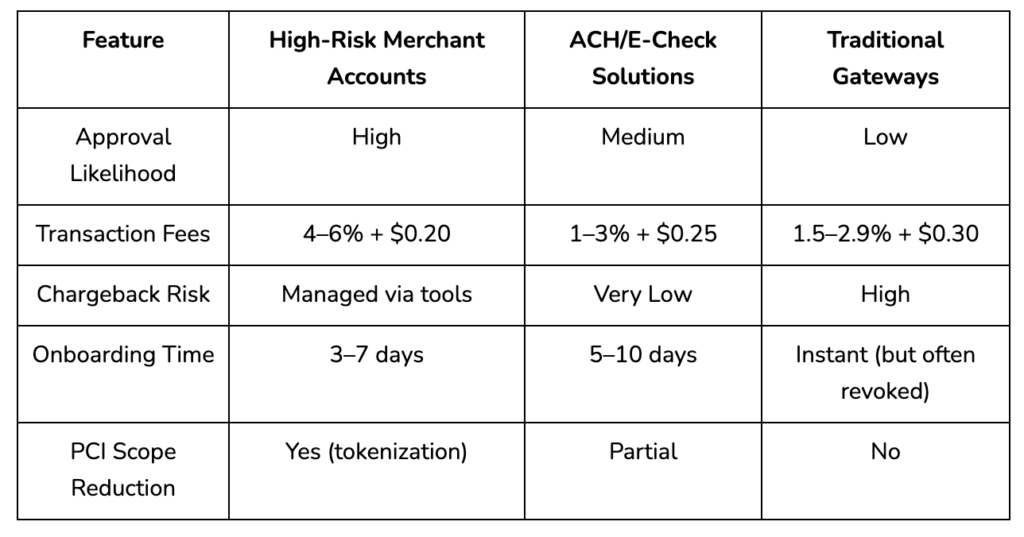

1. High-Risk Merchant Accounts

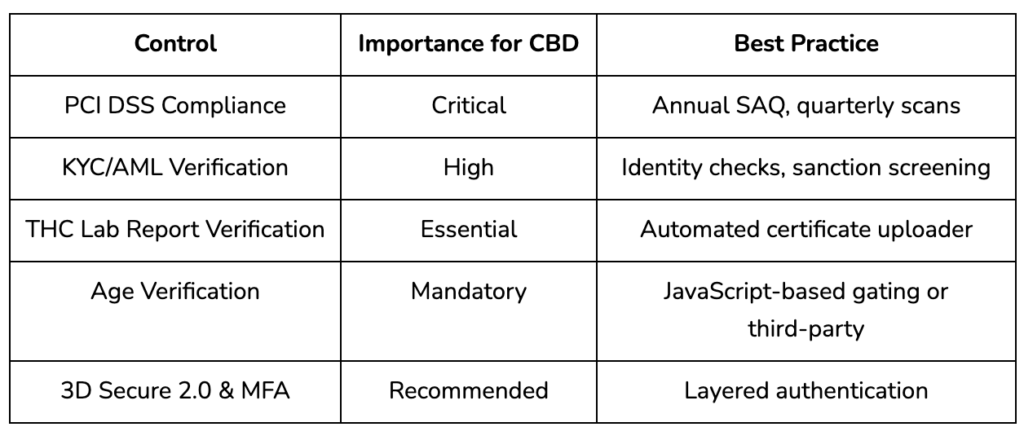

Specialized merchant services know how to underwrite a CBD business. They dig into your compliance certificates, THC lab reports, and business model. Once approved, you benefit from:

- Transaction rates around 4–6%.

- KYC and AML protocols baked into onboarding.

- Chargeback management tools customized for CBD.

2. ACH & E-Check Processing

Moving away from card networks, ACH transfers bypass some card-brand restrictions. Key benefits:

- Lower fees (often 1–3%).

- Reduced chargeback risk.

- Direct bank-to-bank settlement.

The setup requires NACHA compliance and maybe a micro-deposit verification, but it’s a solid fallback when cards fail.

3. Tokenization & Vaulted Credentials

Tokenization encrypts and stores customer payment details off your site, reducing PCI scope. When paired with two-factor authentication and 3D Secure 2.0, you:

- Lower fraud rates.

- Build trust with security-savvy shoppers.

- Qualify for better interchange programs.

What Doesn’t Work: Pitfalls to Avoid

Even in 2025, some solutions promise the moon and deliver headaches:

Traditional Gateways

Big names like Stripe and PayPal still restrict CBD merchants. Despite workarounds, you risk:

- Sudden account termination.

- Frozen funds without notice.

- Hidden repricing after a few months.

Offshore Merchant Accounts

Yes, they sometimes approve CBD quickly, but hidden costs and complex fund routes make reconciliation nightmarish. Compliance audits can escalate if local regulators get involved.

Cash-Only Checkout

Some sites white-label gift cards or cash-on-delivery only. While it evades banking scrutiny, it sacrifices convenience, boosts customer abandonment, and fragments your back-office operations.

How to Get Approved: A Step-by-Step Blueprint

I’ve broken down the journey into manageable milestones:

- Document Readiness Gather:

-

- State or federal hemp licenses

- Third-party lab reports verifying <0.3% THC

- Articles of organization and EIN

- Having these on hand speeds up underwriting.

- Choose a CBD-Friendly Processor Look for providers with experience in seed-to-sale compliance, dedicated account managers, and robust risk scoring.

- Optimize Your Website:

- Add clear disclaimers about product legality.

- Use age-gate verification for 18+ only.

- Display your compliance certificates in the footer.

- Integrate Securely Implement an API-based gateway that supports tokenization, P2PE (point-to-point encryption), and real-time transaction monitoring.

- Test & Validate Run sandbox transactions at various amounts. Confirm settlements and monitor risk flags before going live.

Comparing Top CBD Merchant Services in 2025

Key Compliance & Security Controls

Incorporating Entity-Rich Semantics

When optimizing content, I naturally weave in related entities so search engines understand context:

- Payment gateway API

- Fraud detection algorithms

- Chargeback mitigation strategies

- P2PE and token vault architecture

- ACH routing number validation

- PCI-certified merchant boarding

- Dynamic descriptor management

- Transaction monitoring dashboards

- Regulatory compliance frameworks

The Role of Traditional vs. High-Risk Processing

Some merchants initially pursue Traditional Payment Don’t Work for CBD Businesses, only to hit a wall with suspended accounts. Transitioning to high-risk processors means embracing stronger underwriting yet gaining continuity.

In contrast, niche CBD merchant services offer industry-specific underwriting questionnaires, ensuring your hemp tincture or topical lotion operation sails through review.

Scaling Internationally

If you’re aiming beyond the U.S., consider:

- Multi-currency acquiring

- Local settlement in USD, EUR, GBP, CAD

- Cross-border fee reconciliation

- AML screening per jurisdiction

A global processor built for hemp rather than a generic bank simplifies this expansion.

Seamless Checkout UX for CBD Sales

Nothing kills conversion like a confusing payment flow. Here’s what I implement:

- Consolidated checkout page (no redirects)

- Guest checkout with optional account creation

- Saved-card vaulting with clear opt-in

- Visible security badges (PCI, encryption)

- Real-time declines handling with routing fallback

Positioning Your Brand for Long-Term Success

Securing payment approval isn’t a one-and-done task. Regulations evolve, fraud tactics change, and customer expectations rise. Here’s my long-term strategy:

- Quarterly compliance audits.

- Ongoing lab testing for each new SKU.

- Fraud rule adjustments based on chargeback reports.

- Biannual integration reviews—API updates, token standards.

- Customer support training on payment issues.

I often direct readers to deeper resources, like Payment Processing for CBD & Hemp, to explore niche merchant services. Later, when discussing risk profiles, I point to High-Risk Payment Processing for an in-depth guide on account underwriting.

Final Thoughts

Choosing the right CBD payment solution in 2025 involves striking a balance between security, compliance, user experience, and cost. When I onboard a new client, I assess their product mix, transaction volume, and growth strategy to recommend a tailored stack—often a blend of a specialized merchant account, ACH fallback, and tokenization layer.

For premium cbd payment solutions and end-to-end support, including onboarding, compliance, and ongoing risk management, look no further than Cathedral Payment. We power your online CBD business payments, so you focus on growth.

FAQs

1. How do I accept payments for CBD products online?

I recommend starting with a processor specializing in high-risk industries, providing THC lab reports and KYC documentation to secure a merchant account.

2. Why are CBD merchant services more expensive?

CBD merchants face a higher risk of chargebacks and regulatory scrutiny, so processors charge 4–6% to offset compliance, underwriting, and fraud-prevention costs.

3. Can I use Stripe or PayPal for CBD payments?

Not reliably. While some workarounds exist, these platforms often suspend CBD accounts without warning. Dedicated CBD payment solutions are more stable.

4. What is the average approval time for CBD merchant accounts?

Expect 3–7 business days for specialized high-risk providers. ACH and e-check setups can take up to 10 days due to bank verifications.

5. How do ACH payments compare to credit card processing?

ACH offers lower fees (1–3%) and minimal chargeback risk, but has slower settlement (2-3 days) and requires NACHA compliance and bank account verification.